When Saying Yes Has Cost You Enough: A Financial and Emotional Guide to Setting Limits as a Repeat Guarantor

There is a particular kind of financial exhaustion that does not show up on any balance sheet. It accumulates gradually — the first time you co-signed a car loan for your younger sibling, the lease you guaranteed for your adult child, the personal loan you backed for a cousin going through a rough patch. Each individual decision felt like the right thing to do. Taken together, they may have quietly placed your own financial security in a position of significant vulnerability.

This is the reality facing a growing number of Americans, particularly within immigrant families, multigenerational households, and tight-knit communities where financial interdependence is both a cultural norm and a genuine survival strategy. The problem is not generosity itself — the problem is what happens when generosity becomes reflexive, when the expectation of a "yes" is so deeply embedded in a relationship that the word "no" feels like a form of abandonment.

Recognizing that you have reached your limit — and learning to communicate that boundary clearly and compassionately — is not a betrayal of your values. It is an act of financial self-preservation that ultimately protects both you and the people you care about.

Understanding the Real Exposure of Repeated Guarantorship

Before addressing the relational dimensions of this challenge, it is worth being precise about what repeated co-signing and guarantorship actually means for your financial standing.

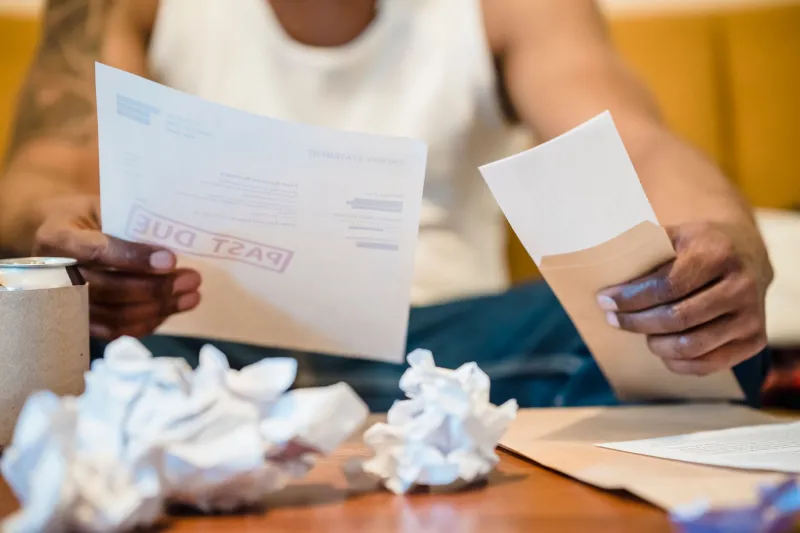

Every obligation you have guaranteed is, from a lender's perspective, your obligation. It appears on your credit report as a liability. When you apply for your own mortgage, auto loan, or line of credit, underwriters factor in all of your guaranteed debts — not just the ones you are personally repaying. This can reduce your effective borrowing capacity significantly, even if every guaranteed account is in good standing.

The risk compounds when a borrower you have backed falls behind on payments. A single missed payment on an account you co-signed can damage your credit score just as severely as a missed payment on your own account. And if the primary borrower defaults entirely, you become the lender's next call — legally obligated to cover the outstanding balance.

For individuals approaching retirement, this exposure carries an additional dimension. Guaranteed debts that go into default can trigger collection actions, judgments, and wage garnishment at precisely the stage of life when financial stability matters most.

Recognizing the Warning Signs of Overextension

Guarantor fatigue rarely announces itself clearly. It tends to build beneath the surface until a triggering event — a missed payment, a new request, a financial review with an advisor — forces the issue into focus. The following signals merit serious attention:

- You have guaranteed three or more active accounts for different borrowers simultaneously.

- You have declined to apply for credit you needed because you were concerned about how your guaranteed obligations would affect your application.

- You feel a sense of dread, rather than care, when a family member contacts you about a financial matter.

- Your own emergency fund or retirement contributions have been disrupted by a guaranteed debt that went into default.

- You have been asked to guarantee a new obligation before a previous one has been resolved.

If two or more of these statements resonate, it is worth conducting a full audit of your current guaranteed obligations with a financial advisor or credit counselor before taking on any new commitments.

How to Say No Without Saying "I Don't Care About You"

The most difficult aspect of setting limits as a guarantor is rarely the financial calculation — it is the conversation. In many families and communities, a refusal to co-sign carries an implicit message about the depth of the relationship. Navigating that perception requires both clarity and compassion.

Start with honesty about your own situation. One of the most effective approaches is to make your refusal about your circumstances rather than a judgment of the other person's creditworthiness. Consider language such as:

"I want to help you, and I need to be honest with you about where I stand. I've been reviewing my finances, and I have more guaranteed debt than I should carry right now. If something went wrong, I wouldn't be able to absorb it — and that would hurt both of us."

This framing accomplishes two things: it removes the implicit criticism of the requester's reliability, and it introduces the concept that your refusal is itself a form of protection for the relationship.

Offer alternatives instead of a flat refusal. A "no" that comes with a constructive alternative is significantly easier to receive than a simple denial. Some options worth considering:

- Connect the person to a credit-building program or secured credit product that can help them qualify independently over time.

- Suggest a community development financial institution (CDFI) or credit union that specializes in working with borrowers who have limited credit histories.

- Offer to help them prepare their application materials or understand their credit report — support that does not require you to assume legal liability.

- Explore whether a smaller, direct financial contribution (a gift or personal loan between individuals) might address the immediate need without creating a formal guaranteed obligation.

Be consistent and calm when the conversation escalates. In some cases, the person asking will push back — expressing hurt, frustration, or appeals to loyalty. It is important to hold the boundary without escalating the emotional temperature. Repeating a simple, consistent message tends to be more effective than defending or elaborating:

"I understand this is disappointing, and I genuinely wish I were in a position to help in this way. I'm not, and that's not going to change right now. I do want to help you find another path forward."

Protecting What You Have Already Built

For those who have already accumulated multiple guarantor obligations, the priority should shift toward risk mitigation. Begin by pulling your full credit reports from all three bureaus and identifying every co-signed or guaranteed account. Assess the payment status of each, and initiate a direct conversation with each primary borrower about the current standing of their account and their plan for managing it going forward.

If any guaranteed accounts are showing signs of stress — irregular payments, approaching balloon amounts, or a borrower who has become unresponsive — consult with a financial advisor or attorney before the situation deteriorates further. In some cases, refinancing the underlying debt in the primary borrower's name alone may be possible if their credit has improved since the original guarantee was made.

Finally, revisit your own retirement and savings trajectory with a clear picture of your current guaranteed liability. The goal is not to feel guilty about past decisions — it is to make future decisions from a position of full information.

Generosity Has a Sustainable Form

At Zaamin, we recognize that financial security is rarely built in isolation. For many Americans, the support of family and community has been the difference between financial stability and genuine hardship. That reality does not diminish — it simply requires that the support be structured in ways that do not silently erode the foundation of the very people providing it.

Setting limits as a guarantor is not the end of your role as a source of support for the people you love. It is the beginning of a more sustainable version of that role — one that you can maintain for years to come, without quietly sacrificing your own future in the process.