When Loyalty Becomes a Liability: The Hidden Wealth Drain of Guarantor Culture in Communities of Color

Across Black, Latino, and immigrant communities throughout the United States, the act of vouching for a neighbor, cousin, or fellow congregation member has long been treated as something close to a moral obligation. Community bonds are real, and the instinct to extend a hand when someone cannot access conventional lending is both admirable and deeply human. But a growing body of evidence suggests that this culture of informal credit support is quietly eroding generational wealth—one defaulted guarantee at a time.

The phenomenon has no formal name in most economic literature, but practitioners in community finance have begun calling it the "guarantor burden." It describes the disproportionate frequency with which individuals from marginalized communities are asked to co-sign, vouch for, or otherwise guarantee the financial obligations of people within their social networks. And when those arrangements fail, the consequences are rarely distributed equally.

The Structural Roots of an Informal System

To understand why this pattern persists, it helps to understand why so many Americans in underserved communities are shut out of conventional credit markets in the first place. According to the Consumer Financial Protection Bureau, approximately 26 million Americans are "credit invisible," meaning they have no credit file at all. Tens of millions more carry files too thin to generate a reliable score. These populations are heavily concentrated among Black and Hispanic households, recent immigrants, and residents of low-income zip codes.

When traditional lenders decline an application, borrowers do not simply abandon their financial needs. They turn to the people around them. A first-generation college student cannot secure an apartment lease without a guarantor; a small business owner cannot qualify for a commercial loan; a young couple cannot rent a car for a family emergency. In each case, the solution often involves asking someone within the community—someone who has managed, often through considerable sacrifice, to build a modest credit profile—to put their name on the line.

This is where the informal transfer begins.

A Wealth Transfer Hidden in Plain Sight

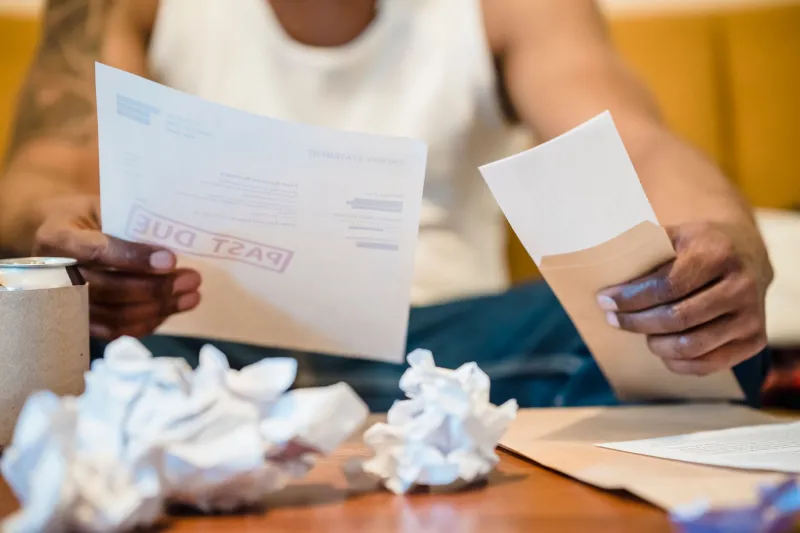

When a guaranteed obligation defaults, the financial damage does not stay with the primary borrower. It migrates directly to the guarantor. A missed rent payment becomes a collections account on the guarantor's credit report. A defaulted personal loan triggers legal liability that can result in wage garnishment or asset seizure. In extreme cases, a guarantor who has spent years building home equity can find that equity threatened by a judgment stemming from someone else's financial collapse.

The critical distinction here is that this kind of wealth erosion does not appear in conventional discussions of the racial wealth gap. Analysts frequently examine disparities in homeownership rates, stock market participation, and inheritance. They rarely account for the quiet subtraction that occurs when a guarantor absorbs a default. Yet the math is unambiguous: every dollar lost to a guarantee is a dollar that cannot be invested, saved, or passed to the next generation.

Research from the Urban Institute and other policy organizations has documented that median Black and Hispanic household wealth remains a fraction of median white household wealth—figures that have changed little over the past three decades despite periods of economic growth. The guarantor burden, while not the sole cause of this disparity, functions as one of many structural mechanisms that keep those gaps from closing.

The Social Architecture of Obligation

What makes this dynamic particularly difficult to address is that it operates through relationships rather than institutions. The person asking for a guarantee is rarely a stranger. She is a sister, a longtime friend, a fellow parishioner. The request carries the full weight of community belonging, and declining it can feel like a betrayal.

Margarita, a 54-year-old administrative assistant in Houston, agreed to guarantee her nephew's car loan in 2019. She describes the conversation as lasting less than ten minutes. "He needed the car to get to work. I had good credit. It felt like the obvious thing to do." When her nephew lost his job during the pandemic and the payments stopped, Margarita found herself fielding calls from a collections agency and watching her credit score drop by more than 80 points. "I had been working on that score for fifteen years," she says. "It was gone in about six months."

Her story is not unusual. Financial counselors working in majority-minority communities report that guarantor-related credit damage is among the most common issues they encounter—and among the hardest to remediate, because the damage typically arrives without warning and compounds quickly.

The Generational Dimension

The long-term implications extend well beyond the individuals directly involved. Credit scores affect access to housing, employment, insurance rates, and the ability to borrow for future needs. A guarantor whose score is damaged in their forties or fifties may find that their capacity to assist their own children—with education, a first home, a business venture—has been materially reduced. The wealth that might have been transferred downward has instead been transferred sideways, absorbed by someone else's default.

This is the generational dimension of the guarantor burden: it does not merely harm the individual who signs the document. It alters the financial trajectory of the entire household and, by extension, the household's children. In communities already navigating systemic barriers to wealth accumulation, these compounding losses are especially consequential.

Toward Structural Alternatives

The solution is not to discourage mutual aid or community solidarity. These are genuine strengths, and the instinct to support one another has real economic value. The challenge is to build formal structures that channel that solidarity without concentrating the risk on individuals who can least afford to absorb it.

Several models are worth examining. Credit unions in underserved communities have experimented with group lending structures that distribute risk across multiple members rather than placing it entirely on a single guarantor. Community development financial institutions, or CDFIs, offer credit-building products designed specifically for borrowers with thin files, reducing the need for personal guarantors in the first place. And some fintech platforms are developing alternative underwriting models that assess creditworthiness through non-traditional data—rent payments, utility bills, employment history—rather than relying solely on FICO scores.

Platforms like Zaamin exist precisely at this intersection: providing structured credit solutions that reduce the need for informal, unprotected guarantee arrangements while offering financial security products designed for communities that conventional lenders have historically overlooked.

Naming the Problem Is the First Step

For too long, the guarantor burden has been invisible in policy conversations about racial wealth inequality. It does not appear on balance sheets. It rarely generates headlines. It unfolds quietly, in kitchens and parking lots and text message threads, one signed document at a time.

But invisibility is not the same as insignificance. The cumulative effect of thousands of informal guarantee arrangements—each one entered into with the best of intentions, many of them ending in financial harm—represents a meaningful drag on wealth accumulation in communities that are already running uphill.

Recognizing this pattern for what it is—a structural feature of an inequitable financial system, not a personal failing of individuals who simply trusted the wrong person—is the first step toward addressing it. The communities absorbing this burden did not create the conditions that made informal guarantees necessary. They deserve financial systems sophisticated enough to meet their needs without asking them to risk everything they have built.