Preying on Trust: How Lenders Exploit Family Bonds to Lock Vulnerable Borrowers Into Guarantor Agreements

When Maria Gutierrez's son needed a personal loan to cover medical expenses, the lender's representative was warm, patient, and seemingly understanding. He explained that because her son had limited credit history, a guarantor — specifically a family member — would make the application process far smoother. Maria, a naturalized citizen with years of steady employment, signed the paperwork without fully grasping what she had agreed to. Eighteen months later, her son defaulted, and the lender came after her savings.

"Nobody explained what it really meant," Maria told a housing counselor who later reviewed her case. "They made it sound like I was just helping him apply."

Maria's story is not an outlier. It is, according to consumer advocates and financial counselors working in underserved communities across the United States, a recognizable and repeating pattern — one that raises serious questions about how certain lenders deliberately design and market guarantor requirements to populations least equipped to understand the legal weight of what they are signing.

The Deliberate Architecture of Dependency

Guarantor lending, in principle, serves a legitimate function. It allows borrowers without established credit histories to access financing by having a creditworthy individual vouch for their ability to repay. In practice, however, the structure creates an asymmetric risk arrangement that can be — and frequently is — exploited.

Consumer finance researchers have documented a pattern in which lenders operating in communities with strong collective financial cultures, particularly among first- and second-generation immigrant households, Latino families, South Asian communities, and multigenerational African American households, disproportionately require guarantors even when the primary borrower's financial profile might qualify them for independent lending elsewhere.

"There is a segment of the lending industry that has mapped out which ZIP codes, which ethnic communities, which churches and social networks are most likely to produce compliant guarantors," says one financial literacy educator based in Los Angeles who asked not to be named due to ongoing relationships with lenders. "They are not doing this accidentally. The marketing is targeted."

The mechanism is straightforward: lenders identify borrowers from communities where saying no to a family member carries significant social and emotional cost. They then present the guarantor requirement not as a risk indicator, but as a routine procedural step — something every family does, something that demonstrates solidarity and support.

Psychological Tactics Designed to Normalize Risk

The language used during loan consultations in these cases is rarely clinical or alarming. Consumer protection attorneys who have reviewed transcripts and recorded calls describe a consistent playbook.

First, the guarantor requirement is framed as a formality rather than a significant legal obligation. Phrases such as "just in case" or "it's mostly paperwork" minimize the perceived stakes. Second, the emotional dimension of family support is activated — representatives frequently reference the borrower's needs in terms that appeal to parental or sibling duty. Third, time pressure is introduced: approvals are described as contingent on same-day or next-day decisions, limiting the guarantor's opportunity to seek independent legal or financial advice.

"What these lenders understand is that in many communities, the instinct to protect family overrides the instinct to protect yourself," explains Dr. Renata Osei, a behavioral economist who has studied financial decision-making in immigrant households. "They are not selling a loan product. They are selling a narrative of loyalty, and the loan is attached to that narrative."

This approach is particularly effective because it converts a financial decision into a moral one. Declining to serve as a guarantor becomes, in the framing the lender constructs, an act of abandonment rather than a sound financial judgment.

The Legal Reality Most Guarantors Never Hear

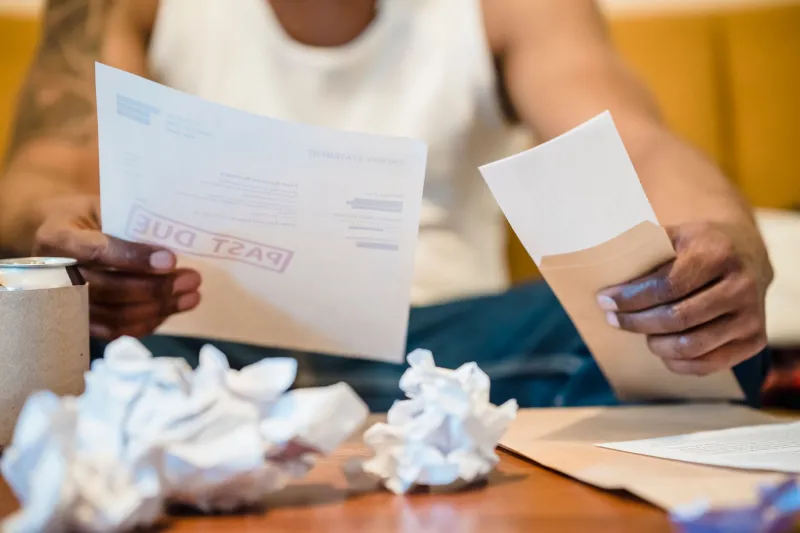

What many guarantors do not fully understand at the point of signing is the scope of their legal exposure. A guarantor is not merely a reference or a character witness. They are a co-obligor — legally responsible for the full amount of the debt if the primary borrower fails to pay. In many states, lenders are not even required to exhaust collection efforts against the primary borrower before pursuing the guarantor.

This means a parent who signs as guarantor on their adult child's $15,000 personal loan can find themselves facing collection calls, wage garnishment proceedings, or damage to their credit score — sometimes before they are even aware the primary borrower has missed a payment.

Federal disclosure requirements under the Truth in Lending Act apply to certain aspects of consumer credit agreements, but advocates argue the existing framework does not adequately ensure that guarantors receive plain-language explanations of their full liability. Several states have enacted additional consumer protections, but enforcement remains inconsistent, and lenders operating across state lines can sometimes structure agreements to minimize regulatory exposure.

Recognizing the Warning Signs

For individuals who are approached about serving as a guarantor, consumer finance advocates recommend treating the request with the same scrutiny one would apply to taking out a loan in one's own name — because that is, effectively, what the commitment represents.

Several warning signs suggest a guarantor arrangement may be structured in bad faith or presented in a misleading way:

- Pressure to decide quickly. Any lender discouraging a guarantor from taking time to review documents or consult an attorney should be viewed with skepticism.

- Vague explanations of liability. If a representative cannot clearly articulate what happens to the guarantor in a default scenario, that is a significant red flag.

- No written summary of obligations. Legitimate lenders provide clear documentation. Reluctance to provide written explanations in plain English is concerning.

- Guarantor requirements that seem disproportionate to the loan size. Requiring a family member to pledge assets or co-sign for a modest loan amount may indicate the lender has already assessed the primary borrower as a high default risk.

- Marketing materials in languages other than English that omit key liability disclosures. This is a documented practice in some markets and may constitute a violation of the Equal Credit Opportunity Act.

Building Protective Habits Before You Sign

For communities where family financial interdependence is both a cultural norm and a genuine source of resilience, the goal is not to dismantle collective support systems but to ensure those systems cannot be weaponized by predatory lenders.

Financial counselors working in these communities recommend several protective practices. Requesting a full copy of all loan documents at least 48 hours before signing is a reasonable and legal right. Consulting a HUD-approved housing counselor or nonprofit credit counselor — many of whom offer free services — before agreeing to any guarantor arrangement can provide critical independent perspective. Community development financial institutions, or CDFIs, and credit unions often offer alternative lending products specifically designed to serve borrowers without strong credit histories, reducing the need for family guarantors altogether.

Platforms such as Zaamin exist precisely to address this gap — offering credit solutions and financial security products that do not require families to gamble with one another's financial stability in order to access basic financing.

A System That Needs Scrutiny

The guarantor requirement, when implemented transparently and ethically, can genuinely expand access to credit for those who need it most. But when it is deployed as a tool to extract value from communities defined by their loyalty to one another, it becomes something else entirely.

The families most likely to be targeted are also, frequently, the families with the least access to independent legal advice, the least familiarity with US consumer protection frameworks, and the greatest cultural pressure to say yes. That convergence is not coincidental. It is, as the evidence increasingly suggests, a feature of how certain lending products are designed.

Recognizing the architecture of that design is the first step toward dismantling it — and toward building financial systems that treat family solidarity as something to be protected, not exploited.